We have taken on several clients in the last few months who were not aware of their automatic enrolment – workplace pension duties which are governed by The Pension Regulator and would have incurred fines had we not stepped in on their behalf so we thought we would outline employers responsibilities.

What Is Automatic Enrolment - Workplace Pension Duties

If you employ at least one person, you are an employer and have certain legal duties. Under the Pensions Act 2008, every employer in the UK must put certain staff into a workplace pension scheme and pay into this, this is called 'automatic enrolment'.

Starting Automatic Enrolment For The First Time

Your legal duties begin on the day your first member of staff starts work which is known as your duties start date. Even if you think you won't need to put your staff into a scheme, you'll still have duties which includes completing an online declaration of compliance to tell The Pension

Regulator what you've done for automatic enrolment.

Duties Start Date

It is recommended that you assess your staff prior to them starting to ensure you are ready for your responsibilities once they have started. Once you have employed your first member of staff, you have to check if they should be enrolled in to a workplace pension.

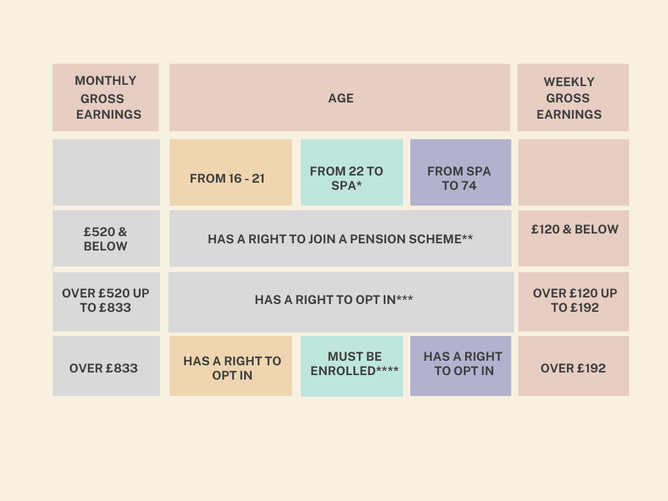

Who Needs To Be Enrolled

These figures are likely to change each year but as of April 2022:

*SPA = State Pension Age

** Has a right to join a pension scheme = if they ask to join a pension scheme, the employer must provide a pension scheme for them, but the employer doesn’t have to pay contributions into a pension scheme.

*** Has a right to opt in = if they ask to be put into a pension scheme, the employer must put them in a pension scheme that can be used for automatic enrolment and pay regular contributions.

**** Must be enrolled = the employer must put these members of staff into a pension scheme that can be used for automatic enrolment and pay regular contributions. The employer doesn't need to ask their permission. If a member of staff gives notice, or the employer gives them notice, to leave employment before the employer has completed this process, the employer has a choice whether to enrol them or not. The employer also has a choice whether to enrol a director who meets these age and earnings criteria.

Pension Scheme

You will need to either set up a new scheme or check your existing scheme meets certain criteria.

After your duties come into effect, your staff (including those on variable pay, flexible pay, irregular hours, etc) should be enrolled the first time they earn over the automatic enrolment threshold of £192* a week or £833* per month if paid monthly.

Once staff have been enrolled, the employer must pay regular contributions into their pension scheme. If the staff member's earnings fall below £120 per week or £520 per month, you may stop paying contributions unless the rules of the pension scheme they have enrolled into require them to continue. You should check with the pension scheme what their rules are.

*Valid September 2022.

Writing To Your Staff

Once staff have been assessed to work out who to put into a pension scheme they must be given information which explains how automatic enrolment applies to them. Within six weeks of the start of your legal duties, you must write to each member of staff who:

Being Enrolled

Explaining what has been done and provide details of the pension scheme chosen for them.

Not Being Enrolled

To let them know they have a right to opt in or join a pension scheme that can be used for automatic enrolment explaining how this would apply to them. Templates can be found by clicking here.

Ongoing Duties

Each time you pay your staff (including new starters), you must monitor their age and earnings to see if they need to be put into a pension scheme and how much you need to pay in.

Every three years you must carry out re-enrolment to put back in any staff who have left your scheme. You’ll need to put staff back into your pension scheme if they have left it, and if they meet the criteria to be put into a pension scheme (known as re-enrolment). The Pension Regulator will write to you in advance of your re-enrolment date to explain more however you must remember to keep your dashboard up-to-date, we have seen so many clients not receive the reminder because they had not updated their address.

You will also need to continue paying into your pension scheme, manage requests to join or leave the scheme and keep records.

Your re-declaration of compliance is an online form for you to tell us how you have met your legal duties.

Even if someone else (such as a bookkeeper) has helped you with your duties, and may even be completing the re-declaration for you, it is your legal duty as the employer to make sure that the re-declaration is completed on time and the information entered is correct. If not, you may be subject to fines.

More Information

Opting out, opting in and joining a scheme

It's against the law to try and persuade staff to opt out of (or leave) a pension scheme, coercing or inducing to opt out can be fined up to £10k. If you don’t have anyone to enrol, you'll still have other duties.

Fines

There are certain legal duties that must be met for automatic enrolment, if you don’t comply with your duties, The Pension Regulator may take enforcement action. If you comply late, you will be expected to pay back any missed contributions to put staff in the position they would have been in if you had complied on time; this would include backdating contributions to the day that your staff member first met the age and earnings criteria to be put into a scheme. When backdating contributions, you must pay all the unpaid employer contributions and your staff member must pay theirs, unless you choose to pay it for them. As part of any enforcement action, they may require that you pay your staff member’s contributions as well as your own.

If you don’t pay your fine, The Pension Regulator can recover the debt through the courts. The most recent data that The Pension regulator has published, in just under 6 months there were over 250 fines with the biggest fine being £52,500.

Prosecution

Wilfully failing to put eligible staff into a pension scheme and knowingly providing false information in a declaration of compliance are criminal offences. The maximum punishment is two years in prison.

How We Can Help

Need help choosing pension scheme? Need help assessing your staff?

We offer The Pension Regulator compliance service as a one off investigation or set up or in addition to our payroll service. Contact us:

Info@cashtrak.co.uk or by clicking here.