Workplace pensions have been around for some time now. Every employer in the UK must put certain staff into a workplace pension scheme and contribute towards it under the Pensions Act 2008. This is called 'automatic enrolment'. If you employ at least one person, you are classed as an employer and as such you have certain legal duties. A business with just a sole director (depending on the circumstances) may be eligible (more to follow below on ‘eligibility’.)

However long your business has been operating, when you take on your first employee, you have automatic enrolment duties that you must comply with straight away. If you employ at least one person, you’re classed as an employer and by law and there are responsibilities you have. These duties apply from first day of employment

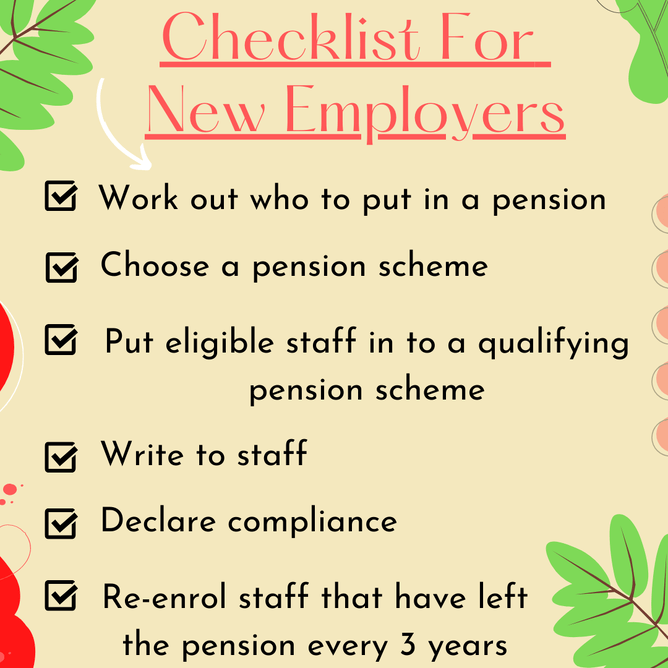

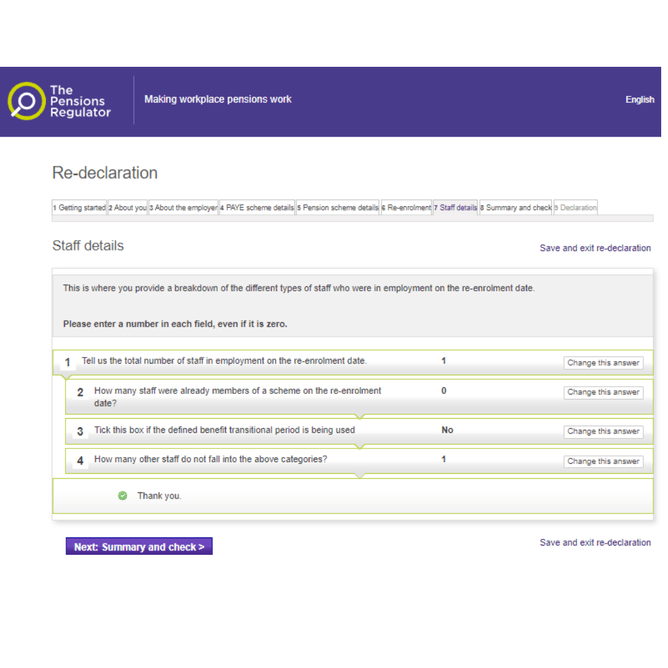

The rules of who is eligible (who should be put in to a workplace pension scheme) can be complicated. In addition to enrolling employees in a workplace pension scheme, every 3 years, you must go through re-enrolment. On top of this, you must complete a declaration of compliance if any employees are eligible, regardless of whether they opt in to the workplace pension. The declaration of compliance needs to be re-declared every 3 years.

Eligiblity

You must carry out a formal assessment to ensure eligible staff are automatically enrolled into a pension scheme. Depending on employees age and earnings, they either:

- Have a right to join a pension scheme – the employer doesn’t have to pay contributions in to a pension scheme but if the employee asks, the employer must provide a pension scheme for them

- Has the right to opt in - if they ask to be put into a pension scheme, the employer must put them in a pension scheme that can be used for automatic enrolment and pay regular contributions.

- Must be enrolled - the employer must put these members of staff into a pension scheme that can be used for automatic enrolment and pay regular contributions. The employer doesn't need to ask their permission. If a member of staff gives notice, or the employer gives them notice to leave employment before the employer has completed this process, the employer has a choice whether to enrol them or not. The employer also has a choice whether to enrol a director who meets these age and earnings criteria.

Assessing Your Employees

This video provides an overview of the criteria to assess employees:

Opting Out, Opting In And Joining A Scheme

It's against the law to try and persuade staff to opt out of (or leave) a pension scheme. Even if you don’t have employees to enrol in a pension, you still have other duties. Fines have been issued to businesses that have tried to get staff not to join the pension.

Employees that have been enrolled and those who have opted in can choose to opt out. You must not actively encourage them to opt out of their workplace pension (which could be considered an inducement), any decision to opt out must be taken freely by the staff member without influence from the employer. The employee can opt out by giving their employer an opt-out notice. The opt-out notice is provided by the pension scheme.

Postponement

You can choose to delay working out who to put into a pension scheme for up to three months for some or all of your staff. This is known as postponement. You must write to your staff to tell them what you are doing and how automatic enrolment applies to them. There are a few reasons you may want to postpone:

- For employees on a probationary period

- Temp or seasonal staff who will not be working past 3 months

Duties

For eligible staff you must:

- Choose a pension scheme

- Assess and work out which employees must go in to a pension scheme

- Write to all employees – regardless if they are to be put in a pension scheme

Writing To Employees

You must write to your employees within 6 weeks after your duties start date. The letters you need to write are as follows:

- Staff who must be put into a pension scheme

- Staff who don't have to be put into a pension scheme

- Staff who are being postponed

Non-Compliance

If you don’t comply with your duties or are found to be persuading your staff to opt out of a pension, The Pension regulator has powers to take enforcement action.

- You, the employer, are responsible for meeting your legal duties for automatic enrolment.

- If you don’t comply, you may face enforcement action including compliance notices, and penalty notices (fines).

- If you comply but after the deadline, you are expected to pay back any missed contributions to put staff in the position they would have been in if you had complied on time; this would include backdating contributions to the day that your staff member first met the age and earnings criteria to be put into a scheme.

- When backdating contributions, you must pay all the unpaid employer contributions and your staff member must pay theirs, unless you choose to pay it for them. As part of any enforcement action we may require that you pay your staff member’s contributions as well as your own.

- If you don’t pay your fine, The Pension Regulator can recover the debt through the courts.

Further Information

The Pension Regulator’s website is full of useful information, checklists and templates however finding what you need can be time consuming and sometimes not straight forward, most businesses will then need to submit a declaration of compliance (regardless of whether there are any employees in a pension) every three years. Click here for The Pension Regulators website. The declaration of compliance can be done by you although again, it is not straight forward. Here are some questions you need to answer:

Some pension providers also require you to do additional submissions every 3 years. There are hefty fines.

How We Can Help

We are still finding a lot of our new clients are unaware of their responsibilities with The Pension Regulator and often don’t realise that The Pension Regulator sees them as an employer even if they are the only member of staff or that they only have part time staff not earning the minimum and are still required to submit a declaration of compliance every 3 years. Whilst The Pension Regulator do send letters to advise businesses of their responsibilities, we have found that their information on businesses can be incorrect or out of date. We have an employer of 10+ eligible staff who are receiving a workplace pension and have done for some time but The Pension Regulator had not realised they were an employer so had not sent any communication. Other businesses we have taken over payroll for have moved and so the communication has not reached them.

As part of our onboarding process we check each business for their responsibilities, for payroll clients we assess them to see if they have any requirements for The Pension regulator. If everything is up to date then they are added to our workflow system to pick up the declaration of compliance to be submitted by the deadline. If there are any issues then we set about resolving this immediately to ensure that no further penalties are issued.

We offer The Pension Regulator service as part of our payroll service or a one off to ensure compliance or to make you compliant.

Contact us today for more information.